Explore Our

“Off The Wall” Blog

Read our Private Wealth Advisory team’s unique thoughts on the markets and investing.

I Was Not Fired

First of all, congratulations to all of the employees at Monument Wealth Management who make this place a pleasure to be at every day. Because of them, we took 10th out of 25 in the Washington Business Journal’s “Best Places to Work” in the Small Business category for the second year in a row (last year we ranked 23rd).

Second, I occasionally really do have to work but I could not pass up an outing at Trump National in D.C. last week. After a fun round with a horrible score, Donald came out on the patio, met our group and took a picture. When he asked me for one piece of investing advice I replied, “Don’t buy a golf course.” He should have hired me years ago when he had the chance…especially since the Dow Jones Industrial Average hit a new all-time high again last week. In all seriousness, the course and club are beautiful.

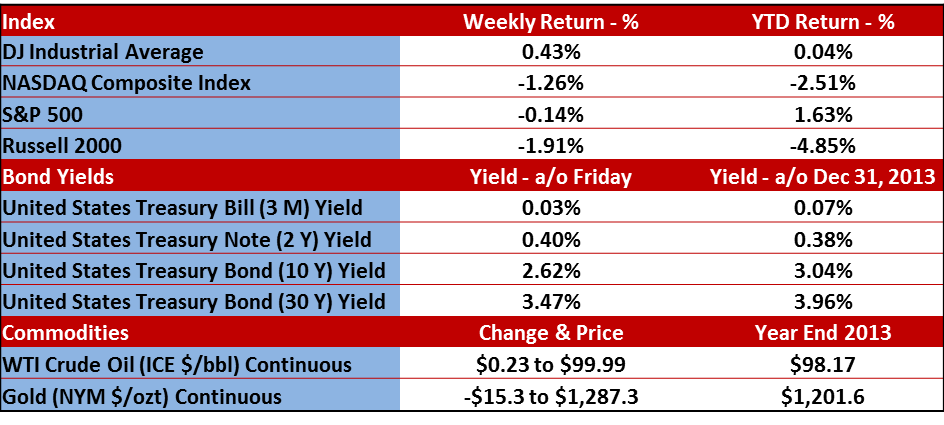

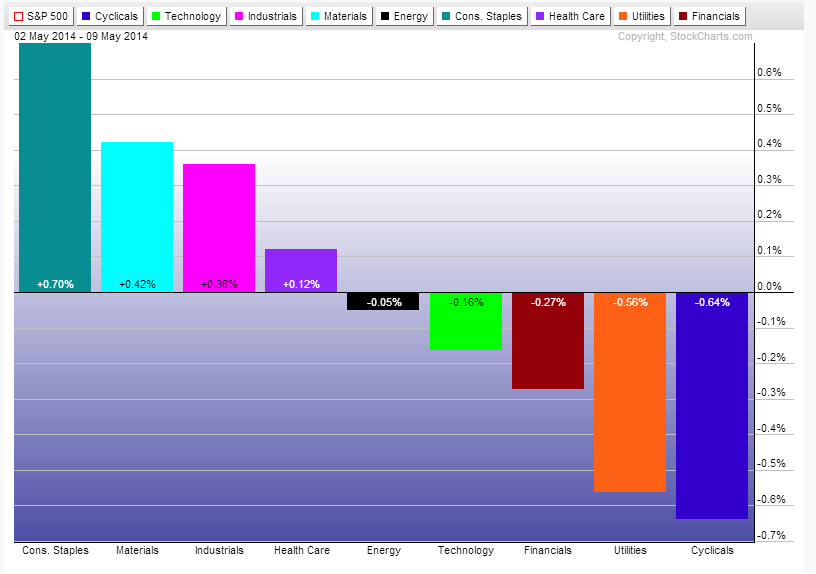

So while the Dow is hitting a new high, the small-caps have been getting HAMMERED! For investors who are well allocated across different equity indices, sizes, styles and sectors, this will probably cause a disconnect between perception and reality. More below, but for now, here is how we fared over the trading week.

Small-Caps – Hammer Time

Small-Caps – Hammer Time

Seriously, name another firm that incorporates MC Hammer lyrics into a finance blog?

The Russell 2000 index (I feel this is the best index to refer to when discussing small-cap stocks) has been HAMMERED over the past month and has basically lost all of the outperformance it had over the S&P 500 since the start of 2013.

Hearken back to March of 2009…the sky was falling and people thought the stock market was heading to zero. Well as we all know now, March 9th marked the low of the crisis and we have been in a bull market ever since…in the S&P 500 that is.

But what about the small-caps? Have they been in a bull market the whole time?

Ummm, technically, no.

Remember that since the current bull market began in March of 2009, the Russell 2000 is currently up around 220% while the S&P 500 is up around 175%.

That’s a big spread …even post this recent hammering.

Now, if we use the common trigger of a bear market (a 20% sell-off), the Russell 2000 index has seen sell-off’s of this magnitude on two different occasions: the summer of 2010 and the fall of 2011.

So that means that investors who believed, in March of 2009, that the economy was recovering/expanding and over-weighted small-caps in lieu of an investment in the S&P 500, experienced excess performance of 45% for every dollar invested in the Russell 2000. HOWEVER, they had to endure two periods when the Russell 2000 technically entered into a bear market correction.

Nothing moves in a straight line and if, as an investor, you held on to your small-caps through the summer of 2010 and the fall of 2011, you can hold on through this correction also. I think the recent sell-off is more an issue to be aware of rather than react to. Nothing earth shattering has happened in the economy (neither positive, nor negative) so to taking action now means despite all of that, doing it would just be following a crowd…

However, if you are looking for a reason, it is probably that the small-cap stocks have been reporting earnings that resemble brown stuff you don’t want to step in. More below.

Earnings

Earnings season ends this week. Here’s where we stand according to Bespoke Investment Group earnings research.

- The percentage of companies beating their revenue estimates for the first quarter of 2014 currently sits at 56.7%, which is basically unchanged from last week. This revenue number is well below the average of 60% which we’ve seen since 2001, but not all that bad when you consider what has happened with actual bottom line earnings.

- The percentage of companies beating their earnings estimates stands at 57.4%, which is a big drop from the 60% one week ago and well off the 61.9% final reading from the fourth quarter of 2013. Last week saw some poor reports from small-cap companies and that accounts for the big move down to 57.4%. Finally, if the number holds at 57.4%, it will represent the worst reading for companies beating their earnings estimates since the bull market began.

They also publish a chart that shows the spread between companies guiding future earnings higher or lower on a percentage basis. Up to this quarter, the spread has been negative for the TEN previous quarters, meaning that there are more companies stating they will earn less in the upcoming quarter than the same quarter a year prior.

As of Friday, the spread between companies posting negative guidance vs. companies posting positive guidance continues to stand at +0.1%. That means, depending on this week, it is possible we could see this reading turn positive for the first quarter in the last 11 quarters.

Finally, in case you missed this last week, our blog got a great write up in Investor’s Business Daily! Check it out here.

Important Disclosure Information for our “Off the Wall” Financial Blog and Market Commentary

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA®

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.