Explore Our

“Off The Wall” Blog

Unique, straight-forward, unfiltered opinion on topics of concern for individuals with newfound wealth.

Trump and the Market – Wrecking Ball

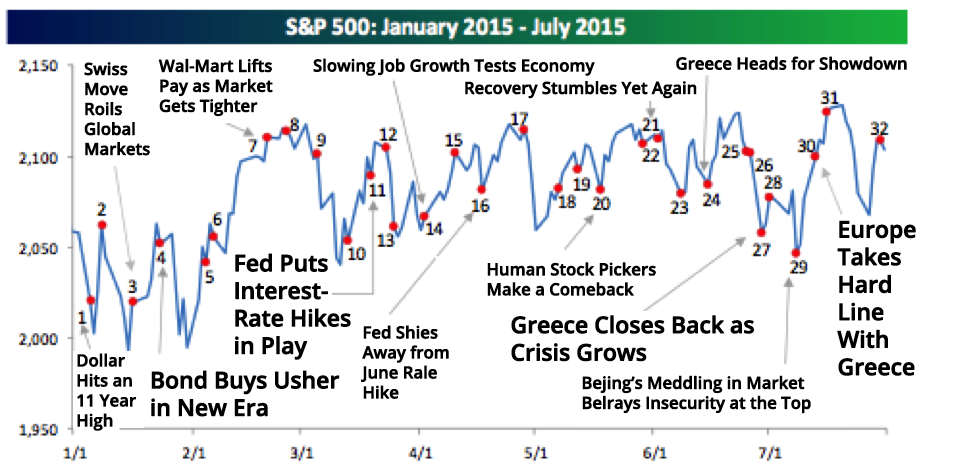

I started my summer vacation last week by traveling to Cleveland to see the GOP debates live. No matter your political party affiliation, being at something like that is really interesting and fun. Trump really came in like a wrecking ball, but Commodities played their role in the market last week, too. After seven straight down sessions for the Dow, which is it’s worst streak since 2011, what’s going on?

For the week, U.S. equities ended lower and there were all kinds of forces at work in the price action of all the indices. Monetary policy, (translation – “The Fed”), remained in focus with the continued back and forth over the timing of the next rate hike and the ambiguity about how much it really means for equity sentiment.

Even though there was a lot of selling off in the equity market this week, economic data continues to come in pretty strong. Consumers are borrowing more than expected, Service industry firms reported strong demand this week, and job numbers show solid growth. Energy (not shockingly) and Consumer Discretionary were the worst performers this week, while Utilities was the only sector to finish in positive territory. Classic defensive action in the market.

As for more details on the economic situation, we saw a solid Employment Report, continued strong auto sales, an increase in consumer credit, a huge positive ISM Services report, and pretty decent manufacturing data. While Construction Spending was off, there were solid upward adjustments to the prior months’ data, and while consumer spending didn’t crush it by any means, it was a healthy pace.

One thing to highlight is that I believe that HUGE components to the economy are Housing and Cars. Auto sales numbers released Monday came in at 17.46 million SAAR (Seasonally Adjusted Annual Rate) versus the 17.2 million expected. We have not seen these kinds of numbers (consistently) on cars since around 2005 and that is when, according to FactSet, there were 24.8 million fewer Americans driving! Then Bespoke reported that the median car today is 11.4 years old, versus 10.0 in 2005. That means there are more Americans today, they are driving more, and their cars are older. Auto sales should keep rising unless there is something like a 9/11 event which no one can predict or hedge against.

One last economy word: the ISM Services report. For anyone out there who is worried about the economy slipping back into a recession … while economists were expecting the ISM Services reading to come in at 56.2, the actual level CRUSHED expectations, coming in at 60.3. That’s not a reading you associate with an economy slipping into dark times. We were just at a nine-year high on this reading back in September of 2014, when it was at 59.6

For those of you worried about the last seven sessions in the Dow, we have had some ups and downs this year. Don’t get all panic-y.

Earnings

Another +1000 companies reported their second quarter (2Q) earnings and revenue last week, bringing the total to almost 2300 companies reporting with just seven days left in this earnings season.

According to Bespoke, here’s how we look:

- The percentage of companies beating their revenue estimates for the 2Q of 2015 stands at 52.7% which is currently well below the average of the 60% that we’ve seen since 2000, but better that the final 50% from the 1Q of 2015.

- Since the revenue readings bottomed out in the 4Q of 2011, quarter-over-quarter readings have ping-ponged but the trend has been positive for revenues, although the last two quarters have been poor. I’ll write more on this at the end of earnings season.

- The percentage of companies beating their earnings estimates stands at 61.1%, which is below the average of 62% dating back to 1998, and above the 60% final reading from the 1Q of 2015.

Bespoke also publishes a chart that shows the spread between companies guiding future earnings higher or lower on a percentage basis. Up until the 1Q of 2014, the spread had been negative for the TEN previous quarters, meaning there were more companies stating they would earn less in the upcoming quarter than the same quarter a year prior. That’s 2.5 years of pessimism coming out of corporate America.

After two flat quarters in the 1Q and 2Q of 2014, we saw the 3Q of 2014 revert back to a negative reading. The final reading for the 4Q of 2014 shows that the spread between companies posting negative guidance versus companies posting positive guidance in the 4Q was a whopping -9.4%! This was the worst spread reading since the last two quarters of 2008. The current reading got a little better over the week moving from -3.5% to -3.0%, which even though it is a negative reading, it’s a huge improvement from the 4Q reading of -9.4%.

Please call or email with questions.

Important Disclosure Information for “Trump and the Market – Wrecking Ball”

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

David B. Armstrong, CFA

President & Co-Founder

Dave got into the industry when he discovered his passion for finance in his mid-20’s. He’s a combat veteran and served as an officer in the United States Marines Corps on both active duty and in the reserves, retiring at the rank of Lieutenant Colonel. While serving on active duty, Dave was unable to spend money on deployments, so he became a self-taught investor. Along with a few bucks cash as a bouncer, his investing performance grew to be good....

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of the Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.