Explore Our

“Off The Wall” Blog

Unique, straight-forward, unfiltered opinion on topics of concern for individuals with newfound wealth.

Lux Libertas

Last week was a sad week for college basketball fans. Dean Smith, the former head coach of the University of North Carolina men’s basketball team, passed away at the age of 83. He was revered by all those who knew him and he was incredibly successful at what he did. You could describe him as the Warren Buffett of coaches – he had only one losing season in 36 years as UNC’s head coach. Can you imagine an investment manager only having one down year in a 36 year stretch? That’s practically unheard of.

If you’ve visited the About Us section on our website recently, you’ll see that our Financial Planning Associate, Ann Schnorrenberg, is a UNC alum. Did you know that she was there when Dean Smith led the Tar Heels and Michael Jordan to their first national championship? MJ, if you’re reading this blog and need wealth management services, please contact us.

Okay, on to the markets. U.S. stocks increased in the first week of February, which was led by the Energy sector. When was the last time you read a sentence like that? It seems like every week it’s just the opposite, since, you know, oil prices have fallen by 50% since June of last year.

Aside from oil, what was behind the rally?

A strong jobs report.

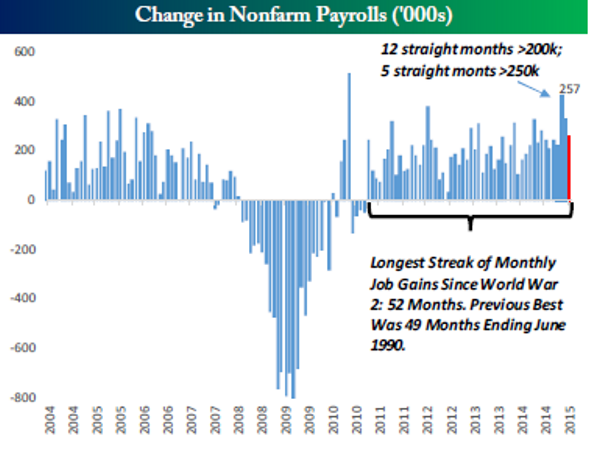

The economy added 257,000 jobs in January, which exceeded analysts’ expectations, and the government also revised the prior two months’ figures upward bringing the job creation for 2014 to 3.12 million. The last time we experienced that kind of growth? The same year that everyone was worrying about the Y2K bug: 1999 when 3.18 million jobs were created.

The chart published by Bespoke Investment Group below shows how many jobs were added or lost each month and it goes back ten years.

{kind=link}

Take a look at the two streaks that we’re currently in the midst of: twelve straight months with over 200,000 jobs added and five straight months with over 250,000 jobs added. More workers means businesses are growing because the economy is getting stronger. More workers also means more people with money in their pockets to buy goods and services. Needless to say, the stock market loves it when you see both of those things occurring.

Earnings

We follow Bespoke Investment Group for earnings research, and here’s where we stand so far in terms of companies that have reported their earnings and revenue for the fourth quarter (4Q) of 2014.

- The percentage of companies beating their revenue estimatesfor the 4Q held steady at 56.7%, which was roughly the same reading from last week and is below the average of 60% that we’ve seen since 2001. As a point of reference, the 3Q of 2014 came in at 57.2% and the 2Q came in at 60.7%. Since the revenue readings bottomed out in the 4Q of 2011, quarter-over-quarter readings have ping-ponged but the trend has been steadily moving UP for revenues.

- The percentage of companies beating their earnings estimatesis at 62.8% which is slightly down from last week’s reading of 63.5%. This is still above the 1% final reading from the 3Q of 2014, and well above the 58.6% final reading from the 2Q of 2014.

Bespoke also publishes a chart that shows the spread between companies guiding future earnings higher or lower on a percentage basis. Up until the 1Q of 2014, the spread had been negative for the TEN previous quarters, meaning there are more companies stating they will earn less in the upcoming quarter than the same quarter a year prior.

Sounds horrible, right? Well maybe not, considering that the S&P 500 was up 46% over that same time period. It seems like CEOs are being overly pessimistic about their earnings outlook.

As of Friday, the spread between companies posting negative guidance versus companies posting positive guidance in the 4Q stood at -9.6%, which would be the lowest reading since the 3Q of 2008. Before you start running for the hills trying to call the top of the market (which we don’t advocate doing), keep in mind that a large portion of the negative guidance is driven by Energy stocks. Stay tuned for a few more weeks to see where the final number comes in.

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Wealth Management), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Monument Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Monument Wealth Management’s current written disclosure statement discussing our advisory services and fees is available for review upon request.

IMPORTANT DISCLOSURE INFORMATION

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Monument Capital Management, LLC [“Monument”]), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Monument. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. No amount of prior experience or success should be construed that a certain level of results or satisfaction will be achieved if Monument is engaged, or continues to be engaged, to provide investment advisory services. Monument is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice.

A copy of the Monument’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request or at www.monumentwealthmanagement.com/disclosures. Please Note: Monument does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Monument’s website or blog or incorporated herein, and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Monument account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Monument accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Remember: If you are a Monument client, please contact Monument, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.